What Is Mortgage Portfolio Risk? A Simple Breakdown

The four risks that wreck mortgage portfolios. Canadian lenders operate without data benchmarks. Here's what portfolio risk means and why it matters.

The four risks that wreck mortgage portfolios. Canadian lenders operate without data benchmarks here's what portfolio risk means and why it matters.

When most people hear "mortgage portfolio risk," their eyes glaze over. I get it.

But if you're a private lender, investment fund manager, or running a PropTech company in Canada, this is the difference between making money and losing your shirt. And right now, most of you are flying blind.

The One-Sentence Version

Mortgage portfolio risk = "What are the chances a bunch of our loans go sideways at the same time, and how bad would that hurt?"

Everything else is just math to answer that question.

Why This Matters

Mortgages aren't like stocks. They're correlated. When housing crashes, it crashes everywhere. When rates spike, everyone feels it. When the economy tanks, defaults cluster.

2008 wasn't random loans failing. It was entire portfolios imploding because nobody understood their risk exposure.

Canada's alternative lending market? Same situation. No data. No benchmarks. Just vibes.

The Four Big Risks

1. Credit Risk

Will they pay you back? Simple question, but it's not about individual defaults. It's about correlated defaults.

100 mortgages to self-employed borrowers in the same city, same industry? When that industry hits trouble, you're toast.

Your 2% default rate sounds great, but compared to what? Without benchmarks, you're guessing.

2. Concentration Risk

Great borrowers. Solid underwriting. Still get destroyed. How?

Too many eggs in one basket.

60% of your portfolio in Toronto condos? When that market softens, math happens. Bad math.

The FDIC has specific thresholds: commercial real estate over 300% of capital triggers alarms. Construction loans at 100% of capital. These aren't random—they're "this is where things historically explode" numbers.

3. Interest Rate Risk

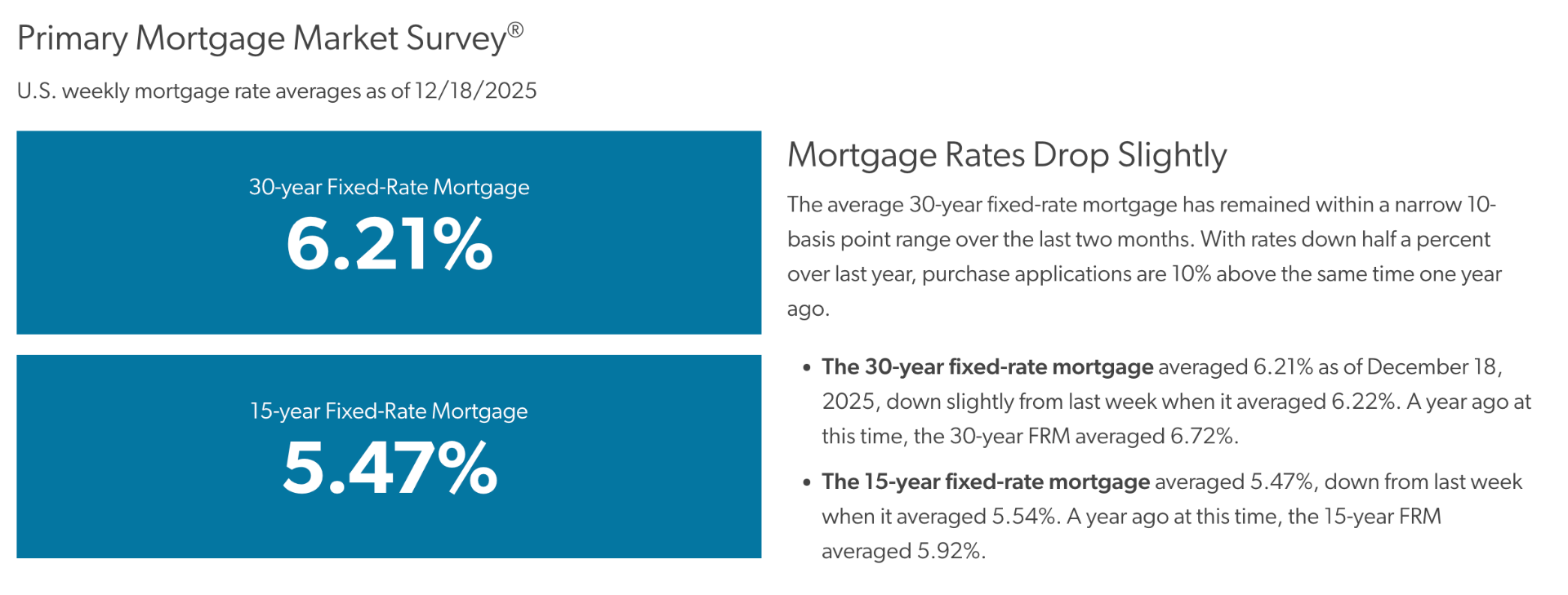

Fixed-rate? Locked in while inflation eats your returns.

Variable-rate? Sweating when rates reset and borrowers can't pay.

You just need to know your exposure and plan for it.

4. Prepayment Risk

"Hey, you got your money back early!" sounds good until you realize you lost years of expected income and now have to redeploy capital in a worse rate environment.

How to Measure It

The basics:

- LTV Ratio: Higher = riskier. 85% average LTV + 10% property drop = underwater loans

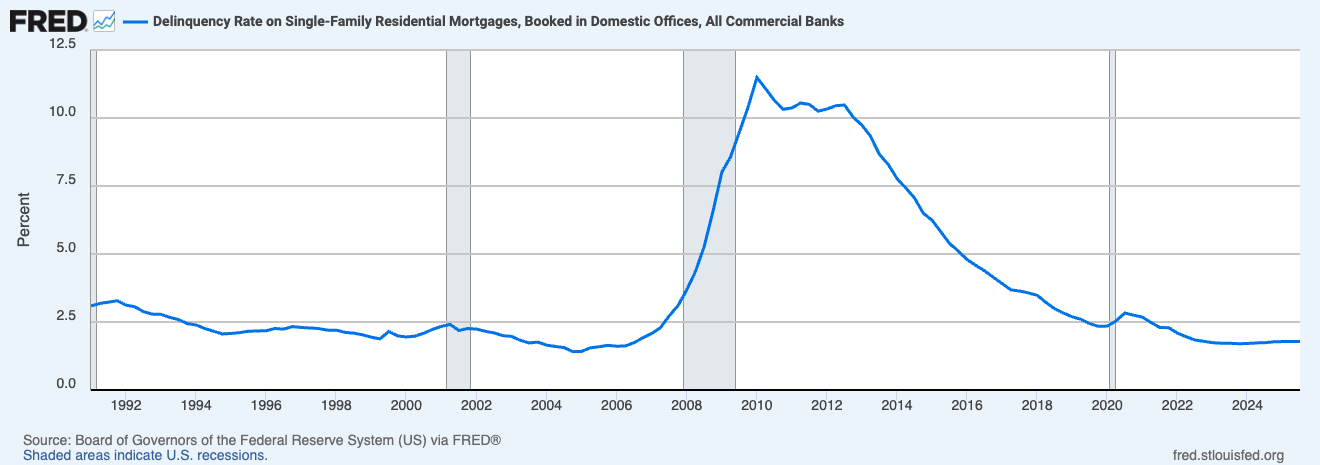

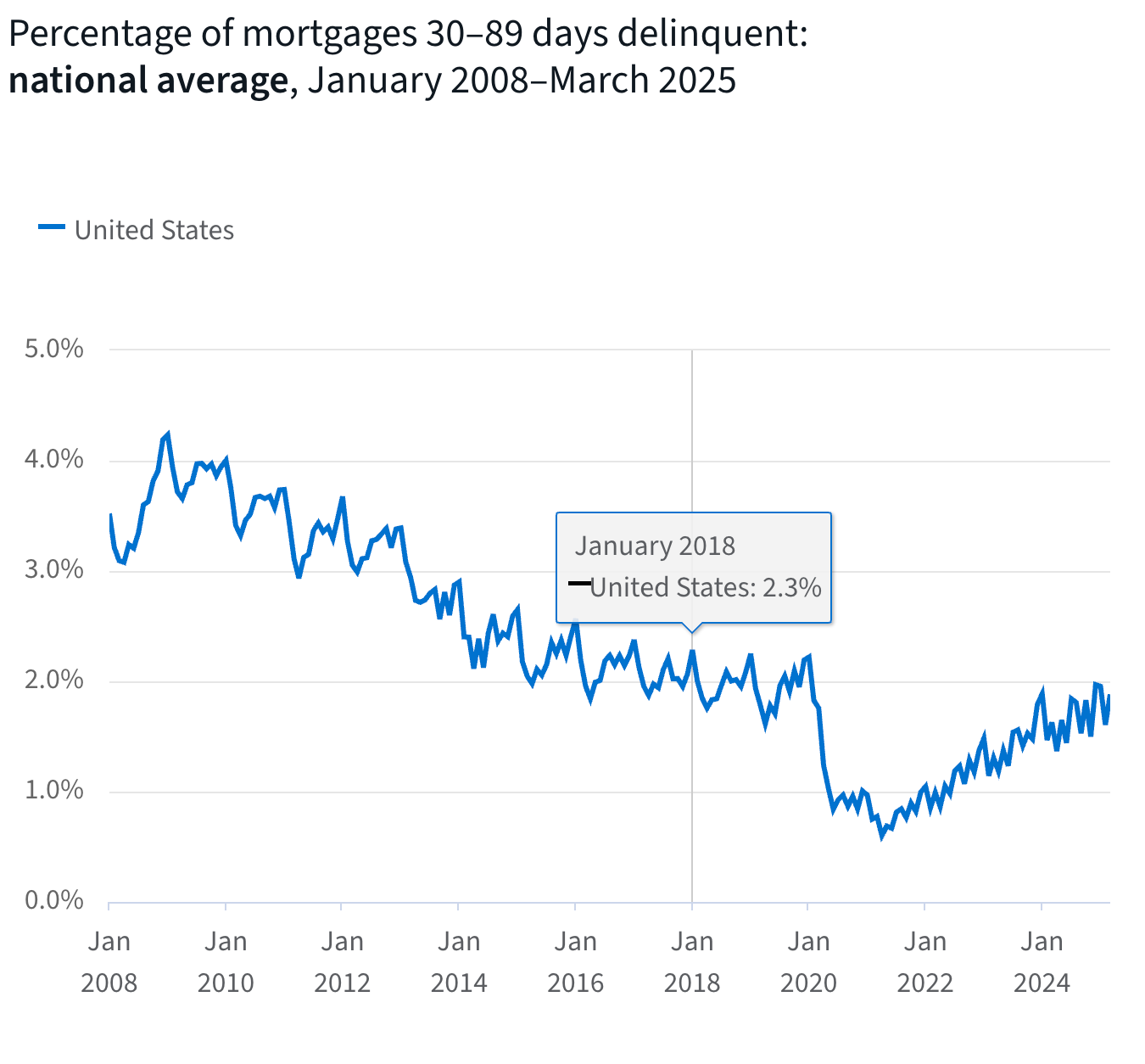

- Delinquency Rate: What % are past due? 30-day vs 90-day tells different stories

- Default Rate: Actually gone sideways. But "default" definitions vary wildly between providers

- Geographic Distribution: 40% in Calgary? Oil industry tanks, you tank

The advanced stuff:

- Stress Testing: Model worst-case scenarios quarterly. "What if property values drop 20%?" If answer is "we're insolvent," fix it now

- Correlation Analysis: Do your loans default together?

- HHI (Concentration Index): Lower = better diversification

The Canadian Problem

In the US: Black Knight and CoreLogic provide real-time data on millions of loans. Default rates by segment. Prepayment speeds. Geographic trends. They make billions because this data is valuable.

In Canada: Nothing. Zero. Zilch.

Bank of Canada releases quarterly reports so aggregated they're useless. CMHC publishes insured mortgage data, but not alternative lending—where the real action is.

So lenders wing it. Multi-million dollar decisions based on gut feel.

- Is your 3% default rate good? Nobody knows.

- Portfolio too concentrated in Ontario? Nobody knows.

- Charging enough for your risk? Nobody knows

What Smart Lenders Do

1. Diversify relentlessly Don't put all loans in one city, one borrower type, one property class. You'll miss peak returns but avoid catastrophe.

2. Track everything Default rates by segment. Average LTV by vintage. Delinquency trends monthly. Geographic concentration. If you can't answer "what's happening" with data, you're gambling.

3. Set limits, enforce them

- "No more than 25% in any metro area"

- "Max 80% average LTV"

- "30% cap on any property type"

When you hit a limit, stop. Yes, even for that hot Vancouver deal.

4. Stress test quarterly Don't wait for crisis to find out if you survive one. Run scenarios before they happen.

5. Build reserves when you can You'll thank yourself when defaults cluster.

Bottom Line

Portfolio risk isn't rocket science. It requires data and discipline.Canada's lenders are making risk decisions in the dark. That's how you get the next crisis. Until that changes, focus on basics: diversify broadly, set conservative limits, stress test regularly, and don't kid yourself about risks. In lending, survival when times get tough beats peak returns when times are good. Too many Canadian lenders are one market correction away from finding out their real risk exposure the hard way.